Debt Serfdom in One Chart

The essence of debt serfdom is debt rises to compensate for stagnant wages.Charles Hugh Smith

Friday, May 04, 2012

I often speak of debt serfdom; here it is, captured in a single chart. The basic dynamics are all here, if you read between the lines:

1. Financialization of the U.S. and global economies diverts income to

capital and those benefitting from globalization/ "financial

innovation;" income for the top 5% rises spectacularly in real terms

even as wages stagnate or decline for the bottom 80%.

2. Previously middle class households (or those who perceive themselves

as middle class) compensate for stagnating incomes and rising costs by

borrowing money: credit cards, auto loans, student loans, etc. In

effect, debt is substituted for income.

3. The dot-com/Internet boom boosted incomes across the board, enabling the bottom 95% to deleverage some of the debt.

4. When the investment/speculation bubble popped, incomes again

declined, and households borrowed heavily against their primary asset,

the home, via home equity lines of credit (HELOCs), second mortgages,

etc.

5. The incomes of the top 5% rose enough that these households could

actually reduce their debt (deleverage) even before the housing bubble

popped.

Here is a chart of real (inflation-adjusted) incomes, courtesy of

analyst Doug Short: note that the incomes of the bottom 80% have been

flatlined for decades, while the top 20% saw modest growth that vanished

once the housing bubble popped. Only the top 5% experienced significant

expansion of income. Notice that incomes of the top 20% and top 5%

really took off in 1982, once financialization became the dominant force

in the economy.

Interestingly, we can see the double-bubble (dot-com and housing)

clearly in the top income brackets, as these speculative bubbles boosted

capital gains and speculation-based income. Since the bottom 80% had

little capital to play with, the twin bubbles barely registered in their

incomes.

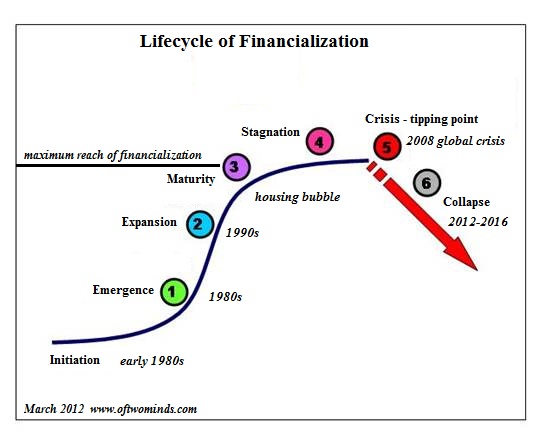

Bottom line: financialization and substituting debt for income have

run their course. They're not coming back, no matter how hard the

Federal Reserve pushes on the string.Both of these interwined trends have traced S-curves and are now in terminal decline:

Those hoping the economy is "recovering" on the backs of financial

speculation/ legerdemain and ramped up borrowing by the lower 95% will

be profoundly disappointed when reality trumps fantasy.

Changes in the definition of AGI in the 1980's caused the IRS to issue a warning that AGI data before the mid-1980's should NOT be compared to AGI after 1990. Many changes to tax reporting rules made the incomes of the top 20% appear to grow more rapidly than they actually did. Another major change in the 1980's was the result of Reagan's greatly reduced personal tax rates: Many small business owners began to include their business income on their personal tax returns, rather than on separate corporate tax returns (where tax rates were now higher). This reporting change made it appear the rich were getting a lot richer, when in fact their previously "invisible" corporate income was now added to their personal tax returns. The mean household income chart you posted IRS warning, and is therefore inaccurate. In addition, the actual people in the top 5% change a lot over a decade -- the top 5% are not the same people every year. I advise you to look up regular reports done by the IRS posted on their website that study income data for the THE SAME PEOPLE over a ten year period, to better understand actual income mobility (studied with the proper methodology). It's very important in economics to start with raw data, and then question the accuracy of the data, rather than starting with a personal belief, and then searching for data to support that belief (aka data mining).

ReplyDeleteI do agree, however, the excessive debt crisis is not over -- moving excessive debt from the private sector to the public sector & central banks, as in the past few years, doesn't eliminate the excessive debt problem! One sign the debt crisis is over, I suspect, would be when banking becomes a safe boring business again, where highly leveraged gambling is avoided, not encouraged. EconomicLogic@yahoo.com